More on Personal Growth

Leon Ho

3 years ago

Digital Brainbuilding (Your Second Brain)

The human brain is amazing. As more scientists examine the brain, we learn how much it can store.

The human brain has 1 billion neurons, according to Scientific American. Each neuron creates 1,000 connections, totaling over a trillion. If each neuron could store one memory, we'd run out of room. [1]

What if you could store and access more info, freeing up brain space for problem-solving and creativity?

Build a second brain to keep up with rising knowledge (what I refer to as a Digital Brain). Effectively managing information entails realizing you can't recall everything.

Every action requires information. You need the correct information to learn a new skill, complete a project at work, or establish a business. You must manage information properly to advance your profession and improve your life.

How to construct a second brain to organize information and achieve goals.

What Is a Second Brain?

How often do you forget an article or book's key point? Have you ever wasted hours looking for a saved file?

If so, you're not alone. Information overload affects millions of individuals worldwide. Information overload drains mental resources and causes anxiety.

This is when the second brain comes in.

Building a second brain doesn't involve duplicating the human brain. Building a system that captures, organizes, retrieves, and archives ideas and thoughts. The second brain improves memory, organization, and recall.

Digital tools are preferable to analog for building a second brain.

Digital tools are portable and accessible. Due to these benefits, we'll focus on digital second-brain building.

Brainware

Digital Brains are external hard drives. It stores, organizes, and retrieves. This means improving your memory won't be difficult.

Memory has three components in computing:

Recording — storing the information

Organization — archiving it in a logical manner

Recall — retrieving it again when you need it

For example:

Due to rigorous security settings, many websites need you to create complicated passwords with special characters.

You must now memorize (Record), organize (Organize), and input this new password the next time you check in (Recall).

Even in this simple example, there are many pieces to remember. We can't recognize this new password with our usual patterns. If we don't use the password every day, we'll forget it. You'll type the wrong password when you try to remember it.

It's common. Is it because the information is complicated? Nope. Passwords are basically letters, numbers, and symbols.

It happens because our brains aren't meant to memorize these. Digital Brains can do heavy lifting.

Why You Need a Digital Brain

Dual minds are best. Birth brain is limited.

The cerebral cortex has 125 trillion synapses, according to a Stanford Study. The human brain can hold 2.5 million terabytes of digital data. [2]

Building a second brain improves learning and memory.

Learn and store information effectively

Faster information recall

Organize information to see connections and patterns

Build a Digital Brain to learn more and reach your goals faster. Building a second brain requires time and work, but you'll have more time for vital undertakings.

Why you need a Digital Brain:

1. Use Brainpower Effectively

Your brain has boundaries, like any organ. This is true while solving a complex question or activity. If you can't focus on a work project, you won't finish it on time.

Second brain reduces distractions. A robust structure helps you handle complicated challenges quickly and stay on track. Without distractions, it's easy to focus on vital activities.

2. Staying Organized

Professional and personal duties must be balanced. With so much to do, it's easy to neglect crucial duties. This is especially true for skill-building. Digital Brain will keep you organized and stress-free.

Life success requires action. Organized people get things done. Organizing your information will give you time for crucial tasks.

You'll finish projects faster with good materials and methods. As you succeed, you'll gain creative confidence. You can then tackle greater jobs.

3. Creativity Process

Creativity drives today's world. Creativity is mysterious and surprising for millions worldwide. Immersing yourself in others' associations, triggers, thoughts, and ideas can generate inspiration and creativity.

Building a second brain is crucial to establishing your creative process and building habits that will help you reach your goals. Creativity doesn't require perfection or overthinking.

4. Transforming Your Knowledge Into Opportunities

This is the age of entrepreneurship. Today, you can publish online, build an audience, and make money.

Whether it's a business or hobby, you'll have several job alternatives. Knowledge can boost your economy with ideas and insights.

5. Improving Thinking and Uncovering Connections

Modern career success depends on how you think. Instead of overthinking or perfecting, collect the best images, stories, metaphors, anecdotes, and observations.

This will increase your creativity and reveal connections. Increasing your imagination can help you achieve your goals, according to research. [3]

Your ability to recognize trends will help you stay ahead of the pack.

6. Credibility for a New Job or Business

Your main asset is experience-based expertise. Others won't be able to learn without your help. Technology makes knowledge tangible.

This lets you use your time as you choose while helping others. Changing professions or establishing a new business become learning opportunities when you have a Digital Brain.

7. Using Learning Resources

Millions of people use internet learning materials to improve their lives. Online resources abound. These include books, forums, podcasts, articles, and webinars.

These resources are mostly free or inexpensive. Organizing your knowledge can save you time and money. Building a Digital Brain helps you learn faster. You'll make rapid progress by enjoying learning.

How does a second brain feel?

Digital Brain has helped me arrange my job and family life for years.

No need to remember 1001 passwords. I never forget anything on my wife's grocery lists. Never miss a meeting. I can access essential information and papers anytime, anywhere.

Delegating memory to a second brain reduces tension and anxiety because you'll know what to do with every piece of information.

No information will be forgotten, boosting your confidence. Better manage your fears and concerns by writing them down and establishing a strategy. You'll understand the plethora of daily information and have a clear head.

How to Develop Your Digital Brain (Your Second Brain)

It's cheap but requires work.

Digital Brain development requires:

Recording — storing the information

Organization — archiving it in a logical manner

Recall — retrieving it again when you need it

1. Decide what information matters before recording.

To succeed in today's environment, you must manage massive amounts of data. Articles, books, webinars, podcasts, emails, and texts provide value. Remembering everything is impossible and overwhelming.

What information do you need to achieve your goals?

You must consolidate ideas and create a strategy to reach your aims. Your biological brain can imagine and create with a Digital Brain.

2. Use the Right Tool

We usually record information without any preparation - we brainstorm in a word processor, email ourselves a message, or take notes while reading.

This information isn't used. You must store information in a central location.

Different information needs different instruments.

Evernote is a top note-taking program. Audio clips, Slack chats, PDFs, text notes, photos, scanned handwritten pages, emails, and webpages can be added.

Pocket is a great software for saving and organizing content. Images, videos, and text can be sorted. Web-optimized design

Calendar apps help you manage your time and enhance your productivity by reminding you of your most important tasks. Calendar apps flourish. The best calendar apps are easy to use, have many features, and work across devices. These calendars include Google, Apple, and Outlook.

To-do list/checklist apps are useful for managing tasks. Easy-to-use, versatility, budget, and cross-platform compatibility are important when picking to-do list apps. Google Keep, Google Tasks, and Apple Notes are good to-do apps.

3. Organize data for easy retrieval

How should you organize collected data?

When you collect and organize data, you'll see connections. An article about networking can assist you comprehend web marketing. Saved business cards can help you find new clients.

Choosing the correct tools helps organize data. Here are some tools selection criteria:

Can the tool sync across devices?

Personal or team?

Has a search function for easy information retrieval?

Does it provide easy data categorization?

Can users create lists or collections?

Does it offer easy idea-information connections?

Does it mind map and visually organize thoughts?

Conclusion

Building a Digital Brain (second brain) helps us save information, think creatively, and implement ideas. Your second brain is a biological extension. It prevents amnesia, allowing you to tackle bigger creative difficulties.

People who love learning often consume information without using it. Every day, they postpone life-improving experiences until they're forgotten. Useful information becomes strength.

Reference

[1] ^ Scientific American: What Is the Memory Capacity of the Human Brain?

[2] ^ Clinical Neurology Specialists: What is the Memory Capacity of a Human Brain?

[3] ^ National Library of Medicine: Imagining Success: Multiple Achievement Goals and the Effectiveness of Imagery

Samer Buna

2 years ago

The Errors I Committed As a Novice Programmer

Learn to identify them, make habits to avoid them

First, a clarification. This article is aimed to make new programmers aware of their mistakes, train them to detect them, and remind them to prevent them.

I learned from all these blunders. I'm glad I have coding habits to avoid them. Do too.

These mistakes are not ordered.

1) Writing code haphazardly

Writing good content is hard. It takes planning and investigation. Quality programs don't differ.

Think. Research. Plan. Write. Validate. Modify. Unfortunately, no good acronym exists. Create a habit of doing the proper quantity of these activities.

As a newbie programmer, my biggest error was writing code without thinking or researching. This works for small stand-alone apps but hurts larger ones.

Like saying anything you might regret, you should think before coding something you could regret. Coding expresses your thoughts.

When angry, count to 10 before you speak. If very angry, a hundred. — Thomas Jefferson.

My quote:

When reviewing code, count to 10 before you refactor a line. If the code does not have tests, a hundred. — Samer Buna

Programming is primarily about reviewing prior code, investigating what is needed and how it fits into the current system, and developing small, testable features. Only 10% of the process involves writing code.

Programming is not writing code. Programming need nurturing.

2) Making excessive plans prior to writing code

Yes. Planning before writing code is good, but too much of it is bad. Water poisons.

Avoid perfect plans. Programming does not have that. Find a good starting plan. Your plan will change, but it helped you structure your code for clarity. Overplanning wastes time.

Only planning small features. All-feature planning should be illegal! The Waterfall Approach is a step-by-step system. That strategy requires extensive planning. This is not planning. Most software projects fail with waterfall. Implementing anything sophisticated requires agile changes to reality.

Programming requires responsiveness. You'll add waterfall plan-unthinkable features. You will eliminate functionality for reasons you never considered in a waterfall plan. Fix bugs and adjust. Be agile.

Plan your future features, though. Do it cautiously since too little or too much planning can affect code quality, which you must risk.

3) Underestimating the Value of Good Code

Readability should be your code's exclusive goal. Unintelligible code stinks. Non-recyclable.

Never undervalue code quality. Coding communicates implementations. Coders must explicitly communicate solution implementations.

Programming quote I like:

Always code as if the guy who ends up maintaining your code will be a violent psychopath who knows where you live. — John Woods

John, great advice!

Small things matter. If your indentation and capitalization are inconsistent, you should lose your coding license.

Long queues are also simple. Readability decreases after 80 characters. To highlight an if-statement block, you might put a long condition on the same line. No. Just never exceed 80 characters.

Linting and formatting tools fix many basic issues like this. ESLint and Prettier work great together in JavaScript. Use them.

Code quality errors:

Multiple lines in a function or file. Break long code into manageable bits. My rule of thumb is that any function with more than 10 lines is excessively long.

Double-negatives. Don't.

Using double negatives is just very not not wrong

Short, generic, or type-based variable names. Name variables clearly.

There are only two hard things in Computer Science: cache invalidation and naming things. — Phil Karlton

Hard-coding primitive strings and numbers without descriptions. If your logic relies on a constant primitive string or numeric value, identify it.

Avoiding simple difficulties with sloppy shortcuts and workarounds. Avoid evasion. Take stock.

Considering lengthier code better. Shorter code is usually preferable. Only write lengthier versions if they improve code readability. For instance, don't utilize clever one-liners and nested ternary statements just to make the code shorter. In any application, removing unneeded code is better.

Measuring programming progress by lines of code is like measuring aircraft building progress by weight. — Bill Gates

Excessive conditional logic. Conditional logic is unnecessary for most tasks. Choose based on readability. Measure performance before optimizing. Avoid Yoda conditions and conditional assignments.

4) Selecting the First Approach

When I started programming, I would solve an issue and move on. I would apply my initial solution without considering its intricacies and probable shortcomings.

After questioning all the solutions, the best ones usually emerge. If you can't think of several answers, you don't grasp the problem.

Programmers do not solve problems. Find the easiest solution. The solution must work well and be easy to read, comprehend, and maintain.

There are two ways of constructing a software design. One way is to make it so simple that there are obviously no deficiencies, and the other way is to make it so complicated that there are no obvious deficiencies. — C.A.R. Hoare

5) Not Giving Up

I generally stick with the original solution even though it may not be the best. The not-quitting mentality may explain this. This mindset is helpful for most things, but not programming. Program writers should fail early and often.

If you doubt a solution, toss it and rethink the situation. No matter how much you put in that solution. GIT lets you branch off and try various solutions. Use it.

Do not be attached to code because of how much effort you put into it. Bad code needs to be discarded.

6) Avoiding Google

I've wasted time solving problems when I should have researched them first.

Unless you're employing cutting-edge technology, someone else has probably solved your problem. Google It First.

Googling may discover that what you think is an issue isn't and that you should embrace it. Do not presume you know everything needed to choose a solution. Google surprises.

But Google carefully. Newbies also copy code without knowing it. Use only code you understand, even if it solves your problem.

Never assume you know how to code creatively.

The most dangerous thought that you can have as a creative person is to think that you know what you’re doing. — Bret Victor

7) Failing to Use Encapsulation

Not about object-oriented paradigm. Encapsulation is always useful. Unencapsulated systems are difficult to maintain.

An application should only handle a feature once. One object handles that. The application's other objects should only see what's essential. Reducing application dependencies is not about secrecy. Following these guidelines lets you safely update class, object, and function internals without breaking things.

Classify logic and state concepts. Class means blueprint template. Class or Function objects are possible. It could be a Module or Package.

Self-contained tasks need methods in a logic class. Methods should accomplish one thing well. Similar classes should share method names.

As a rookie programmer, I didn't always establish a new class for a conceptual unit or recognize self-contained units. Newbie code has a Util class full of unrelated code. Another symptom of novice code is when a small change cascades and requires numerous other adjustments.

Think before adding a method or new responsibilities to a method. Time's needed. Avoid skipping or refactoring. Start right.

High Cohesion and Low Coupling involves grouping relevant code in a class and reducing class dependencies.

8) Arranging for Uncertainty

Thinking beyond your solution is appealing. Every line of code will bring up what-ifs. This is excellent for edge cases but not for foreseeable needs.

Your what-ifs must fall into one of these two categories. Write only code you need today. Avoid future planning.

Writing a feature for future use is improper. No.

Write only the code you need today for your solution. Handle edge-cases, but don't introduce edge-features.

Growth for the sake of growth is the ideology of the cancer cell. — Edward Abbey

9) Making the incorrect data structure choices

Beginner programmers often overemphasize algorithms when preparing for interviews. Good algorithms should be identified and used when needed, but memorizing them won't make you a programming genius.

However, learning your language's data structures' strengths and shortcomings will make you a better developer.

The improper data structure shouts "newbie coding" here.

Let me give you a few instances of data structures without teaching you:

Managing records with arrays instead of maps (objects).

Most data structure mistakes include using lists instead of maps to manage records. Use a map to organize a list of records.

This list of records has an identifier to look up each entry. Lists for scalar values are OK and frequently superior, especially if the focus is pushing values to the list.

Arrays and objects are the most common JavaScript list and map structures, respectively (there is also a map structure in modern JavaScript).

Lists over maps for record management often fail. I recommend always using this point, even though it only applies to huge collections. This is crucial because maps are faster than lists in looking up records by identifier.

Stackless

Simple recursive functions are often tempting when writing recursive programming. In single-threaded settings, optimizing recursive code is difficult.

Recursive function returns determine code optimization. Optimizing a recursive function that returns two or more calls to itself is harder than optimizing a single call.

Beginners overlook the alternative to recursive functions. Use Stack. Push function calls to a stack and start popping them out to traverse them back.

10) Worsening the current code

Imagine this:

Add an item to that room. You might want to store that object anywhere as it's a mess. You can finish in seconds.

Not with messy code. Do not worsen! Keep the code cleaner than when you started.

Clean the room above to place the new object. If the item is clothing, clear a route to the closet. That's proper execution.

The following bad habits frequently make code worse:

code duplication You are merely duplicating code and creating more chaos if you copy/paste a code block and then alter just the line after that. This would be equivalent to adding another chair with a lower base rather than purchasing a new chair with a height-adjustable seat in the context of the aforementioned dirty room example. Always keep abstraction in mind, and use it when appropriate.

utilizing configuration files not at all. A configuration file should contain the value you need to utilize if it may differ in certain circumstances or at different times. A configuration file should contain a value if you need to use it across numerous lines of code. Every time you add a new value to the code, simply ask yourself: "Does this value belong in a configuration file?" The most likely response is "yes."

using temporary variables and pointless conditional statements. Every if-statement represents a logic branch that should at the very least be tested twice. When avoiding conditionals doesn't compromise readability, it should be done. The main issue with this is that branch logic is being used to extend an existing function rather than creating a new function. Are you altering the code at the appropriate level, or should you go think about the issue at a higher level every time you feel you need an if-statement or a new function variable?

This code illustrates superfluous if-statements:

function isOdd(number) {

if (number % 2 === 1) {

return true;

} else {

return false;

}

}Can you spot the biggest issue with the isOdd function above?

Unnecessary if-statement. Similar code:

function isOdd(number) {

return (number % 2 === 1);

};11) Making remarks on things that are obvious

I've learnt to avoid comments. Most code comments can be renamed.

instead of:

// This function sums only odd numbers in an array

const sum = (val) => {

return val.reduce((a, b) => {

if (b % 2 === 1) { // If the current number is odd

a+=b; // Add current number to accumulator

}

return a; // The accumulator

}, 0);

};Commentless code looks like this:

const sumOddValues = (array) => {

return array.reduce((accumulator, currentNumber) => {

if (isOdd(currentNumber)) {

return accumulator + currentNumber;

}

return accumulator;

}, 0);

};Better function and argument names eliminate most comments. Remember that before commenting.

Sometimes you have to use comments to clarify the code. This is when your comments should answer WHY this code rather than WHAT it does.

Do not write a WHAT remark to clarify the code. Here are some unnecessary comments that clutter code:

// create a variable and initialize it to 0

let sum = 0;

// Loop over array

array.forEach(

// For each number in the array

(number) => {

// Add the current number to the sum variable

sum += number;

}

);Avoid that programmer. Reject that code. Remove such comments if necessary. Most importantly, teach programmers how awful these remarks are. Tell programmers who publish remarks like this that they may lose their jobs. That terrible.

12) Skipping tests

I'll simplify. If you develop code without tests because you think you're an excellent programmer, you're a rookie.

If you're not writing tests in code, you're probably testing manually. Every few lines of code in a web application will be refreshed and interacted with. Also. Manual code testing is fine. To learn how to automatically test your code, manually test it. After testing your application, return to your code editor and write code to automatically perform the same interaction the next time you add code.

Human. After each code update, you will forget to test all successful validations. Automate it!

Before writing code to fulfill validations, guess or design them. TDD is real. It improves your feature design thinking.

If you can use TDD, even partially, do so.

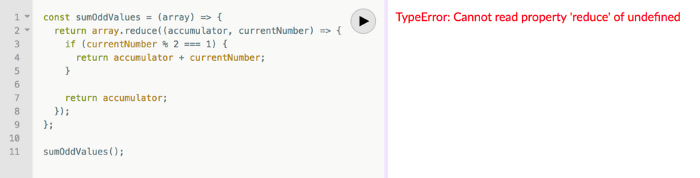

13) Making the assumption that if something is working, it must be right.

See this sumOddValues function. Is it flawed?

const sumOddValues = (array) => {

return array.reduce((accumulator, currentNumber) => {

if (currentNumber % 2 === 1) {

return accumulator + currentNumber;

}

return accumulator;

});

};

console.assert(

sumOddValues([1, 2, 3, 4, 5]) === 9

);Verified. Good life. Correct?

Code above is incomplete. It handles some scenarios correctly, including the assumption used, but it has many other issues. I'll list some:

#1: No empty input handling. What happens when the function is called without arguments? That results in an error revealing the function's implementation:

TypeError: Cannot read property 'reduce' of undefined.

Two main factors indicate faulty code.

Your function's users shouldn't come across implementation-related information.

The user cannot benefit from the error. Simply said, they were unable to use your function. They would be aware that they misused the function if the error was more obvious about the usage issue. You might decide to make the function throw a custom exception, for instance:

TypeError: Cannot execute function for empty list.Instead of returning an error, your method should disregard empty input and return a sum of 0. This case requires action.

Problem #2: No input validation. What happens if the function is invoked with a text, integer, or object instead of an array?

The function now throws:

sumOddValues(42);

TypeError: array.reduce is not a functionUnfortunately, array. cut's a function!

The function labels anything you call it with (42 in the example above) as array because we named the argument array. The error says 42.reduce is not a function.

See how that error confuses? An mistake like:

TypeError: 42 is not an array, dude.Edge-cases are #1 and #2. These edge-cases are typical, but you should also consider less obvious ones. Negative numbers—what happens?

sumOddValues([1, 2, 3, 4, 5, -13]) // => still 9-13's unusual. Is this the desired function behavior? Error? Should it sum negative numbers? Should it keep ignoring negative numbers? You may notice the function should have been titled sumPositiveOddNumbers.

This decision is simple. The more essential point is that if you don't write a test case to document your decision, future function maintainers won't know if you ignored negative values intentionally or accidentally.

It’s not a bug. It’s a feature. — Someone who forgot a test case

#3: Valid cases are not tested. Forget edge-cases, this function mishandles a straightforward case:

sumOddValues([2, 1, 3, 4, 5]) // => 11The 2 above was wrongly included in sum.

The solution is simple: reduce accepts a second input to initialize the accumulator. Reduce will use the first value in the collection as the accumulator if that argument is not provided, like in the code above. The sum included the test case's first even value.

This test case should have been included in the tests along with many others, such as all-even numbers, a list with 0 in it, and an empty list.

Newbie code also has rudimentary tests that disregard edge-cases.

14) Adhering to Current Law

Unless you're a lone supercoder, you'll encounter stupid code. Beginners don't identify it and assume it's decent code because it works and has been in the codebase for a while.

Worse, if the terrible code uses bad practices, the newbie may be enticed to use them elsewhere in the codebase since they learnt them from good code.

A unique condition may have pushed the developer to write faulty code. This is a nice spot for a thorough note that informs newbies about that condition and why the code is written that way.

Beginners should presume that undocumented code they don't understand is bad. Ask. Enquire. Blame it!

If the code's author is dead or can't remember it, research and understand it. Only after understanding the code can you judge its quality. Before that, presume nothing.

15) Being fixated on best practices

Best practices damage. It suggests no further research. Best practice ever. No doubts!

No best practices. Today's programming language may have good practices.

Programming best practices are now considered bad practices.

Time will reveal better methods. Focus on your strengths, not best practices.

Do not do anything because you read a quote, saw someone else do it, or heard it is a recommended practice. This contains all my article advice! Ask questions, challenge theories, know your options, and make informed decisions.

16) Being preoccupied with performance

Premature optimization is the root of all evil (or at least most of it) in programming — Donald Knuth (1974)

I think Donald Knuth's advice is still relevant today, even though programming has changed.

Do not optimize code if you cannot measure the suspected performance problem.

Optimizing before code execution is likely premature. You may possibly be wasting time optimizing.

There are obvious optimizations to consider when writing new code. You must not flood the event loop or block the call stack in Node.js. Remember this early optimization. Will this code block the call stack?

Avoid non-obvious code optimization without measurements. If done, your performance boost may cause new issues.

Stop optimizing unmeasured performance issues.

17) Missing the End-User Experience as a Goal

How can an app add a feature easily? Look at it from your perspective or in the existing User Interface. Right? Add it to the form if the feature captures user input. Add it to your nested menu of links if it adds a link to a page.

Avoid that developer. Be a professional who empathizes with customers. They imagine this feature's consumers' needs and behavior. They focus on making the feature easy to find and use, not just adding it to the software.

18) Choosing the incorrect tool for the task

Every programmer has their preferred tools. Most tools are good for one thing and bad for others.

The worst tool for screwing in a screw is a hammer. Do not use your favorite hammer on a screw. Don't use Amazon's most popular hammer on a screw.

A true beginner relies on tool popularity rather than problem fit.

You may not know the best tools for a project. You may know the best tool. However, it wouldn't rank high. You must learn your tools and be open to new ones.

Some coders shun new tools. They like their tools and don't want to learn new ones. I can relate, but it's wrong.

You can build a house slowly with basic tools or rapidly with superior tools. You must learn and use new tools.

19) Failing to recognize that data issues are caused by code issues

Programs commonly manage data. The software will add, delete, and change records.

Even the simplest programming errors can make data unpredictable. Especially if the same defective application validates all data.

Code-data relationships may be confusing for beginners. They may employ broken code in production since feature X is not critical. Buggy coding may cause hidden data integrity issues.

Worse, deploying code that corrected flaws without fixing minor data problems caused by these defects will only collect more data problems that take the situation into the unrecoverable-level category.

How do you avoid these issues? Simply employ numerous data integrity validation levels. Use several interfaces. Front-end, back-end, network, and database validations. If not, apply database constraints.

Use all database constraints when adding columns and tables:

If a column has a NOT NULL constraint, null values will be rejected for that column. If your application expects that field has a value, your database should designate its source as not null.

If a column has a UNIQUE constraint, the entire table cannot include duplicate values for that column. This is ideal for a username or email field on a Users table, for instance.

For the data to be accepted, a CHECK constraint, or custom expression, must evaluate to true. For instance, you can apply a check constraint to ensure that the values of a normal % column must fall within the range of 0 and 100.

With a PRIMARY KEY constraint, the values of the columns must be both distinct and not null. This one is presumably what you're utilizing. To distinguish the records in each table, the database needs have a primary key.

A FOREIGN KEY constraint requires that the values in one database column, typically a primary key, match those in another table column.

Transaction apathy is another data integrity issue for newbies. If numerous actions affect the same data source and depend on each other, they must be wrapped in a transaction that can be rolled back if one fails.

20) Reinventing the Wheel

Tricky. Some programming wheels need reinvention. Programming is undefined. New requirements and changes happen faster than any team can handle.

Instead of modifying the wheel we all adore, maybe we should rethink it if you need a wheel that spins at varied speeds depending on the time of day. If you don't require a non-standard wheel, don't reinvent it. Use the darn wheel.

Wheel brands can be hard to choose from. Research and test before buying! Most software wheels are free and transparent. Internal design quality lets you evaluate coding wheels. Try open-source wheels. Debug and fix open-source software simply. They're easily replaceable. In-house support is also easy.

If you need a wheel, don't buy a new automobile and put your maintained car on top. Do not include a library to use a few functions. Lodash in JavaScript is the finest example. Import shuffle to shuffle an array. Don't import lodash.

21) Adopting the incorrect perspective on code reviews

Beginners often see code reviews as criticism. Dislike them. Not appreciated. Even fear them.

Incorrect. If so, modify your mindset immediately. Learn from every code review. Salute them. Observe. Most crucial, thank reviewers who teach you.

Always learning code. Accept it. Most code reviews teach something new. Use these for learning.

You may need to correct the reviewer. If your code didn't make that evident, it may need to be changed. If you must teach your reviewer, remember that teaching is one of the most enjoyable things a programmer can do.

22) Not Using Source Control

Newbies often underestimate Git's capabilities.

Source control is more than sharing your modifications. It's much bigger. Clear history is source control. The history of coding will assist address complex problems. Commit messages matter. They are another way to communicate your implementations, and utilizing them with modest commits helps future maintainers understand how the code got where it is.

Commit early and often with present-tense verbs. Summarize your messages but be detailed. If you need more than a few lines, your commit is too long. Rebase!

Avoid needless commit messages. Commit summaries should not list new, changed, or deleted files. Git commands can display that list from the commit object. The summary message would be noise. I think a big commit has many summaries per file altered.

Source control involves discoverability. You can discover the commit that introduced a function and see its context if you doubt its need or design. Commits can even pinpoint which code caused a bug. Git has a binary search within commits (bisect) to find the bug-causing commit.

Source control can be used before commits to great effect. Staging changes, patching selectively, resetting, stashing, editing, applying, diffing, reversing, and others enrich your coding flow. Know, use, and enjoy them.

I consider a Git rookie someone who knows less functionalities.

23) Excessive Use of Shared State

Again, this is not about functional programming vs. other paradigms. That's another article.

Shared state is problematic and should be avoided if feasible. If not, use shared state as little as possible.

As a new programmer, I didn't know that all variables represent shared states. All variables in the same scope can change its data. Global scope reduces shared state span. Keep new states in limited scopes and avoid upward leakage.

When numerous resources modify common state in the same event loop tick, the situation becomes severe (in event-loop-based environments). Races happen.

This shared state race condition problem may encourage a rookie to utilize a timer, especially if they have a data lock issue. Red flag. No. Never accept it.

24) Adopting the Wrong Mentality Toward Errors

Errors are good. Progress. They indicate a simple way to improve.

Expert programmers enjoy errors. Newbies detest them.

If these lovely red error warnings irritate you, modify your mindset. Consider them helpers. Handle them. Use them to advance.

Some errors need exceptions. Plan for user-defined exceptions. Ignore some mistakes. Crash and exit the app.

25) Ignoring rest periods

Humans require mental breaks. Take breaks. In the zone, you'll forget breaks. Another symptom of beginners. No compromises. Make breaks mandatory in your process. Take frequent pauses. Take a little walk to plan your next move. Reread the code.

This has been a long post. You deserve a break.

Tim Denning

3 years ago

In this recession, according to Mark Cuban, you need to outwork everyone

Here’s why that’s baloney

Mark Cuban popularized entrepreneurship.

Shark Tank (which made Mark famous) made starting a business glamorous to attract more entrepreneurs. First off

This isn't an anti-billionaire rant.

Mark Cuban has done excellent. He's a smart, principled businessman. I enjoy his Web3 work. But Mark's work and productivity theories are absurd.

You don't need to outwork everyone in this recession to live well.

You won't be able to outwork me.

Yuck! Mark's words made me gag.

Why do boys think working is a football game where the winner wins a Super Bowl trophy? To outwork you.

Hard work doesn't equal intelligence.

Highly clever professionals spend 4 hours a day in a flow state, then go home to relax with family.

If you don't put forth the effort, someone else will.

- Mark.

He'll burn out. He's delusional and doesn't understand productivity. Boredom or disconnection spark our best thoughts.

TikTok outlaws boredom.

In a spare minute, we check our phones because we can't stand stillness.

All this work p*rn makes things worse. When is it okay to feel again? Because I can’t feel anything when I’m drowning in work and haven’t had a holiday in 2 years.

Your rivals are actively attempting to undermine you.

Ohhh please Mark…seriously.

This isn't a Tom Hanks war film. Relax. Not everyone is a rival. Only yourself is your competitor. To survive the recession, be better than a year ago.

If you get rich, great. If not, there's more to life than Lambos and angel investments.

Some want to relax and enjoy life. No competition. We witness people with lives trying to endure the recession and record-high prices.

This fictitious rival worsens life and work.

If you are truly talented, you will motivate others to work more diligently and effectively.

No Mark. Soz.

If you're a good leader, you won't brag about working hard and treating others like cogs. Treat them like humans. You'll have EQ.

Silly statements like this are caused by an out-of-control ego. No longer watch Shark Tank.

Ego over humanity.

Good leaders will urge people to keep together during the recession. Good leaders support those who are laid off and need a reference.

Not harder, quicker, better. That created my mental health problems 10 years ago.

Truth: we want to work less.

The promotion of entrepreneurship is ludicrous.

Marvel superheroes. Seriously, relax Max.

I used to write about entrepreneurship, then I quit. Many WeWork Adam Neumanns. Carelessness.

I now utilize the side hustle title when writing about online company or entrepreneurship. Humanizes.

Stop glorifying. Thinking we'll all be Elon Musks who send rockets to Mars is delusional. Most of us won't create companies employing hundreds.

OK.

The true epidemic is glorification. fewer selfies Little birdy needs less bank account screenshots. Less Uber talk.

We're exhausted.

Fun, ego-free business can transform the world. Take a relax pill.

Work as if someone were attempting to take everything from you.

I've seen people lose everything.

Myself included. My 20s startup failed. I was almost bankrupt. I thought I'd never recover. Nope.

Best thing ever.

Losing everything reveals your true self. Unintelligent entrepreneur egos perish instantly. Regaining humility revitalizes relationships.

Money's significance shifts. Stop chasing it like a puppy with a bone.

Fearing loss is unfounded.

Here is a more effective approach than outworking nobody.

(You'll thrive in the recession and become wealthy.)

Smarter work

Overworking is donkey work.

You don't want to be a career-long overworker. Instead than wasting time, write down what you do. List tasks and processes.

Keep doing/outsource the list. Step-by-step each task. Continuously systematize.

Then recruit a digital employee like Zapier or a virtual assistant in the same country.

Intelligent, not difficult.

If your big break could burn in hell, diversify like it will.

People err by focusing on one chance.

Chances can vanish. All-in risky. Instead of working like a Mark Cuban groupie, diversify your income.

If you're employed, your customer is your employer.

Sell the same abilities twice and add 2-3 contract clients. Reduce your hours at your main job and take on more clients.

Leave brand loyalty behind

Mark desires his employees' worship.

That's stupid. When times are bad, layoffs multiply. The problem is the false belief that companies care. No. A business maximizes profit and pays you the least.

To care or overpay is anti-capitalist (that run the world). Be honest.

I was a banker. Then the bat virus hit and jobs disappeared faster than I urinate after a night of drinking.

Start being disloyal now since your company will cheerfully replace you with a better applicant. Meet recruiters and hiring managers on LinkedIn. Whenever something goes wrong at work, act.

Loyalty to self and family. Nobody.

Outwork this instead

Mark doesn't suggest outworking inflation instead of people.

Inflation erodes your time on earth. If you ignore inflation, you'll work harder for less pay every minute.

Financial literacy beats inflation.

Get a side job and earn money online

So you can stop outworking everyone.

Internet leverages time. Same effort today yields exponential results later. There are still whole places not online.

Instead of working forever, generate money online.

Final Words

Overworking is stupid. Don't listen to wealthy football jocks.

Work isn't everything. Prioritize diversification, internet income streams, boredom, and financial knowledge throughout the recession.

That’s how to get wealthy rather than burnout-rich.

You might also like

Amelie Carver

3 years ago

Web3 Needs More Writers to Educate Us About It

WRITE FOR THE WEB3

Why web3’s messaging is lost and how crypto winter is growing growth seeds

People interested in crypto, blockchain, and web3 typically read Bitcoin and Ethereum's white papers. It's a good idea. Documents produced for developers and academia aren't always the ideal resource for beginners.

Given the surge of extremely technical material and the number of fly-by-nights, rug pulls, and other scams, it's little wonder mainstream audiences regard the blockchain sector as an expensive sideshow act.

What's the solution?

Web3 needs more than just builders.

After joining TikTok, I followed Amy Suto of SutoScience. Amy switched from TV scriptwriting to IT copywriting years ago. She concentrates on web3 now. Decentralized autonomous organizations (DAOs) are seeking skilled copywriters for web3.

Amy has found that web3's basics are easy to grasp; you don't need technical knowledge. There's a paradigm shift in knowing the basics; be persistent and patient.

Apple is positioning itself as a data privacy advocate, leveraging web3's zero-trust ethos on data ownership.

Finn Lobsien, who writes about web3 copywriting for the Mirror and Twitter, agrees: acronyms and abstractions won't do.

Web3 preached to the choir. Curious newcomers have only found whitepapers and scams when trying to learn why the community loves it. No wonder people resist education and buy-in.

Due to the gender gap in crypto (Crypto Bro is not just a stereotype), it attracts people singing to the choir or trying to cash in on the next big thing.

Last year, the industry was booming, so writing wasn't necessary. Now that the bear market has returned (for everyone, but especially web3), holding readers' attention is a valuable skill.

White papers and the Web3

Why does web3 rely so much on non-growth content?

Businesses must polish and improve their messaging moving into the 2022 recession. The 2021 tech boom provided such a sense of affluence and (unsustainable) growth that no one needed great marketing material. The market found them.

This was especially true for web3 and the first-time crypto believers. Obviously. If they knew which was good.

White papers help. White papers are highly technical texts that walk a reader through a product's details. How Does a White Paper Help Your Business and That White Paper Guy discuss them.

They're meant for knowledgeable readers. Investors and the technical (academic/developer) community read web3 white papers. White papers are used when a product is extremely technical or difficult to assist an informed reader to a conclusion. Web3 uses them most often for ICOs (initial coin offerings).

White papers for web3 education help newcomers learn about the web3 industry's components. It's like sending a first-grader to the Annotated Oxford English Dictionary to learn to read. It's a reference, not a learning tool, for words.

Newcomers can use platforms that teach the basics. These included Coinbase's Crypto Basics tutorials or Cryptochicks Academy, founded by the mother of Ethereum's inventor to get more women utilizing and working in crypto.

Discord and Web3 communities

Discord communities are web3's opposite. Discord communities involve personal communications and group involvement.

Online audience growth begins with community building. User personas prefer 1000 dedicated admirers over 1 million lukewarm followers, and the language is much more easygoing. Discord groups are renowned for phishing scams, compromised wallets, and incorrect information, especially since the crypto crisis.

White papers and Discord increase industry insularity. White papers are complicated, and Discord has a high risk threshold.

Web3 and writing ads

Copywriting is emotional, but white papers are logical. It uses the brain's quick-decision centers. It's meant to make the reader invest immediately.

Not bad. People think sales are sleazy, but they can spot the poor things.

Ethical copywriting helps you reach the correct audience. People who gain a following on Medium are likely to have copywriting training and a readership (or three) in mind when they publish. Tim Denning and Sinem Günel know how to identify a target audience and make them want to learn more.

In a fast-moving market, copywriting is less about long-form content like sales pages or blogs, but many organizations do. Instead, the copy is concise, individualized, and high-value. Tweets, email marketing, and IM apps (Discord, Telegram, Slack to a lesser extent) keep engagement high.

What does web3's messaging lack? As DAOs add stricter copyrighting, narrative and connecting tales seem to be missing.

Web3 is passionate about constructing the next internet. Now, they can connect their passion to a specific audience so newcomers understand why.

Sam Hickmann

3 years ago

Donor-Advised Fund Tax Benefits (DAF)

Giving through a donor-advised fund can be tax-efficient. Using a donor-advised fund can reduce your tax liability while increasing your charitable impact.

Grow Your Donations Tax-Free.

Your DAF's charitable dollars can be invested before being distributed. Your DAF balance can grow with the market. This increases grantmaking funds. The assets of the DAF belong to the charitable sponsor, so you will not be taxed on any growth.

Avoid a Windfall Tax Year.

DAFs can help reduce tax burdens after a windfall like an inheritance, business sale, or strong market returns. Contributions to your DAF are immediately tax deductible, lowering your taxable income. With DAFs, you can effectively pre-fund years of giving with assets from a single high-income event.

Make a contribution to reduce or eliminate capital gains.

One of the most common ways to fund a DAF is by gifting publicly traded securities. Securities held for more than a year can be donated at fair market value and are not subject to capital gains tax. If a donor liquidates assets and then donates the proceeds to their DAF, capital gains tax reduces the amount available for philanthropy. Gifts of appreciated securities, mutual funds, real estate, and other assets are immediately tax deductible up to 30% of Adjusted gross income (AGI), with a five-year carry-forward for gifts that exceed AGI limits.

Using Appreciated Stock as a Gift

Donating appreciated stock directly to a DAF rather than liquidating it and donating the proceeds reduces philanthropists' tax liability by eliminating capital gains tax and lowering marginal income tax.

In the example below, a donor has $100,000 in long-term appreciated stock with a cost basis of $10,000:

Using a DAF would allow this donor to give more to charity while paying less taxes. This strategy often allows donors to give more than 20% more to their favorite causes.

For illustration purposes, this hypothetical example assumes a 35% income tax rate. All realized gains are subject to the federal long-term capital gains tax of 20% and the 3.8% Medicare surtax. No other state taxes are considered.

The information provided here is general and educational in nature. It is not intended to be, nor should it be construed as, legal or tax advice. NPT does not provide legal or tax advice. Furthermore, the content provided here is related to taxation at the federal level only. NPT strongly encourages you to consult with your tax advisor or attorney before making charitable contributions.

Ajay Shrestha

2 years ago

Bitcoin's technical innovation: addressing the issue of the Byzantine generals

The 2008 Bitcoin white paper solves the classic computer science consensus problem.

Issue Statement

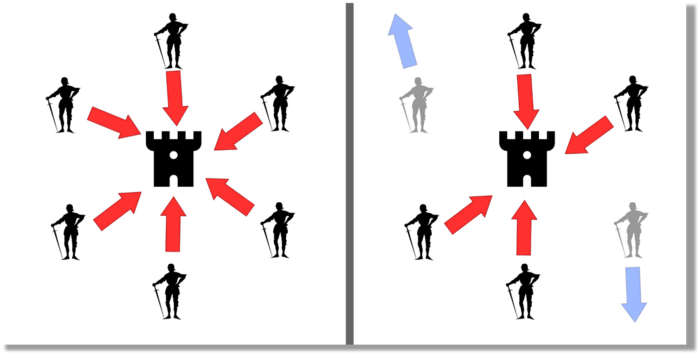

The Byzantine Generals Problem (BGP) is called after an allegory in which several generals must collaborate and attack a city at the same time to win (figure 1-left). Any general who retreats at the last minute loses the fight (figure 1-right). Thus, precise messengers and no rogue generals are essential. This is difficult without a trusted central authority.

In their 1982 publication, Leslie Lamport, Robert Shostak, and Marshall Please termed this topic the Byzantine Generals Problem to simplify distributed computer systems.

Consensus in a distributed computer network is the issue. Reaching a consensus on which systems work (and stay in the network) and which don't makes maintaining a network tough (i.e., needs to be removed from network). Challenges include unreliable communication routes between systems and mis-reporting systems.

Solving BGP can let us construct machine learning solutions without single points of failure or trusted central entities. One server hosts model parameters while numerous workers train the model. This study describes fault-tolerant Distributed Byzantine Machine Learning.

Bitcoin invented a mechanism for a distributed network of nodes to agree on which transactions should go into the distributed ledger (blockchain) without a trusted central body. It solved BGP implementation. Satoshi Nakamoto, the pseudonymous bitcoin creator, solved the challenge by cleverly combining cryptography and consensus mechanisms.

Disclaimer

This is not financial advice. It discusses a unique computer science solution.

Bitcoin

Bitcoin's white paper begins:

“A purely peer-to-peer version of electronic cash would allow online payments to be sent directly from one party to another without going through a financial institution.” Source: https://www.ussc.gov/sites/default/files/pdf/training/annual-national-training-seminar/2018/Emerging_Tech_Bitcoin_Crypto.pdf

Bitcoin's main parts:

The open-source and versioned bitcoin software that governs how nodes, miners, and the bitcoin token operate.

The native kind of token, known as a bitcoin token, may be created by mining (up to 21 million can be created), and it can be transferred between wallet addresses in the bitcoin network.

Distributed Ledger, which contains exact copies of the database (or "blockchain") containing each transaction since the first one in January 2009.

distributed network of nodes (computers) running the distributed ledger replica together with the bitcoin software. They broadcast the transactions to other peer nodes after validating and accepting them.

Proof of work (PoW) is a cryptographic requirement that must be met in order for a miner to be granted permission to add a new block of transactions to the blockchain of the cryptocurrency bitcoin. It takes the form of a valid hash digest. In order to produce new blocks on average every 10 minutes, Bitcoin features a built-in difficulty adjustment function that modifies the valid hash requirement (length of nonce). PoW requires a lot of energy since it must continually generate new hashes at random until it satisfies the criteria.

The competing parties known as miners carry out continuous computing processing to address recurrent cryptography issues. Transaction fees and some freshly minted (mined) bitcoin are the rewards they receive. The amount of hashes produced each second—or hash rate—is a measure of mining capacity.

Cryptography, decentralization, and the proof-of-work consensus method are Bitcoin's most unique features.

Bitcoin uses encryption

Bitcoin employs this established cryptography.

Hashing

digital signatures based on asymmetric encryption

Hashing (SHA-256) (SHA-256)

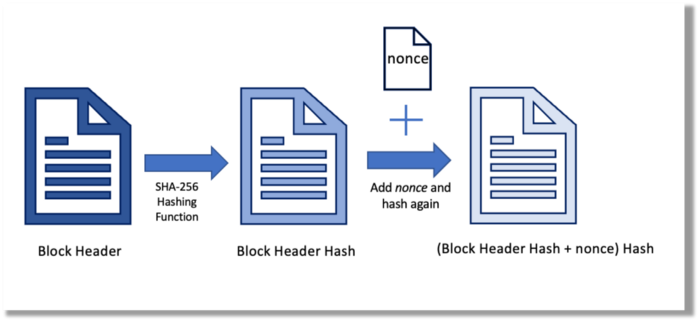

Hashing converts unique plaintext data into a digest. Creating the plaintext from the digest is impossible. Bitcoin miners generate new hashes using SHA-256 to win block rewards.

A new hash is created from the current block header and a variable value called nonce. To achieve the required hash, mining involves altering the nonce and re-hashing.

The block header contains the previous block hash and a Merkle root, which contains hashes of all transactions in the block. Thus, a chain of blocks with increasing hashes links back to the first block. Hashing protects new transactions and makes the bitcoin blockchain immutable. After a transaction block is mined, it becomes hard to fabricate even a little entry.

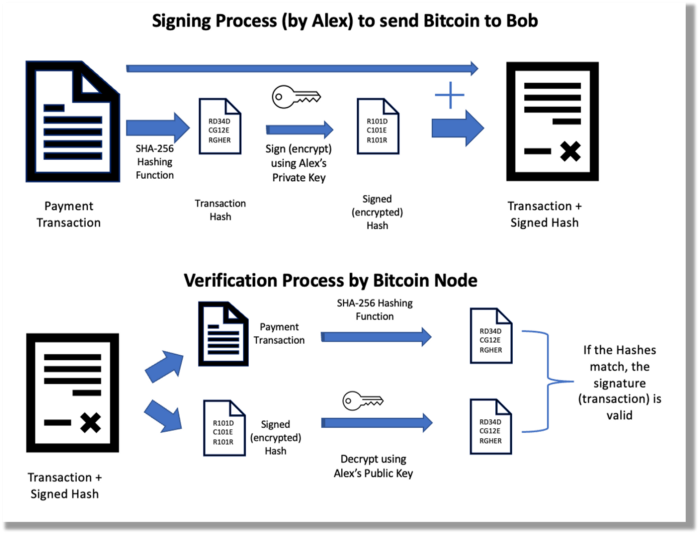

Asymmetric Cryptography Digital Signatures

Asymmetric cryptography (public-key encryption) requires each side to have a secret and public key. Public keys (wallet addresses) can be shared with the transaction party, but private keys should not. A message (e.g., bitcoin payment record) can only be signed by the owner (sender) with the private key, but any node or anybody with access to the public key (visible in the blockchain) can verify it. Alex will submit a digitally signed transaction with a desired amount of bitcoin addressed to Bob's wallet to a node to send bitcoin to Bob. Alex alone has the secret keys to authorize that amount. Alex's blockchain public key allows anyone to verify the transaction.

Solution

Now, apply bitcoin to BGP. BGP generals resemble bitcoin nodes. The generals' consensus is like bitcoin nodes' blockchain block selection. Bitcoin software on all nodes can:

Check transactions (i.e., validate digital signatures)

2. Accept and propagate just the first miner to receive the valid hash and verify it accomplished the task. The only way to guess the proper hash is to brute force it by repeatedly producing one with the fixed/current block header and a fresh nonce value.

Thus, PoW and a dispersed network of nodes that accept blocks from miners that solve the unfalsifiable cryptographic challenge solve consensus.

Suppose:

Unreliable nodes

Unreliable miners

Bitcoin accepts the longest chain if rogue nodes cause divergence in accepted blocks. Thus, rogue nodes must outnumber honest nodes in accepting/forming the longer chain for invalid transactions to reach the blockchain. As of November 2022, 7000 coordinated rogue nodes are needed to takeover the bitcoin network.

Dishonest miners could also try to insert blocks with falsified transactions (double spend, reverse, censor, etc.) into the chain. This requires over 50% (51% attack) of miners (total computational power) to outguess the hash and attack the network. Mining hash rate exceeds 200 million (source). Rewards and transaction fees encourage miners to cooperate rather than attack. Quantum computers may become a threat.

Visit my Quantum Computing post.

Quantum computers—what are they? Quantum computers will have a big influence. towardsdatascience.com

Nodes have more power than miners since they can validate transactions and reject fake blocks. Thus, the network is secure if honest nodes are the majority.

Summary

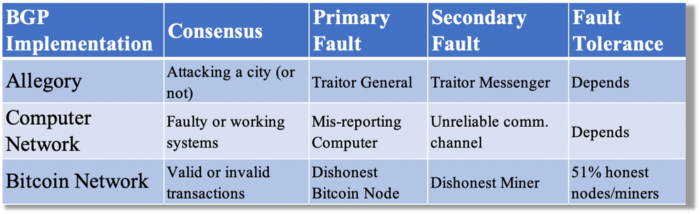

Table 1 compares three Byzantine Generals Problem implementations.

Bitcoin white paper and implementation solved the consensus challenge of distributed systems without central governance. It solved the illusive Byzantine Generals Problem.

Resources

Resources

Source-code for Bitcoin Core Software — https://github.com/bitcoin/bitcoin

Bitcoin white paper — https://bitcoin.org/bitcoin.pdf

https://www.microsoft.com/en-us/research/publication/byzantine-generals-problem/

https://www.microsoft.com/en-us/research/uploads/prod/2016/12/The-Byzantine-Generals-Problem.pdf

Genuinely Distributed Byzantine Machine Learning, El-Mahdi El-Mhamdi et al., 2020. ACM, New York, NY, https://doi.org/10.1145/3382734.3405695