More on Personal Growth

Zuzanna Sieja

3 years ago

In 2022, each data scientist needs to read these 11 books.

Non-technical talents can benefit data scientists in addition to statistics and programming.

As our article 5 Most In-Demand Skills for Data Scientists shows, being business-minded is useful. How can you get such a diverse skill set? We've compiled a list of helpful resources.

Data science, data analysis, programming, and business are covered. Even a few of these books will make you a better data scientist.

Ready? Let’s dive in.

Best books for data scientists

1. The Black Swan

Author: Nassim Taleb

First, a less obvious title. Nassim Nicholas Taleb's seminal series examines uncertainty, probability, risk, and decision-making.

Three characteristics define a black swan event:

It is erratic.

It has a significant impact.

Many times, people try to come up with an explanation that makes it seem more predictable than it actually was.

People formerly believed all swans were white because they'd never seen otherwise. A black swan in Australia shattered their belief.

Taleb uses this incident to illustrate how human thinking mistakes affect decision-making. The book teaches readers to be aware of unpredictability in the ever-changing IT business.

Try multiple tactics and models because you may find the answer.

2. High Output Management

Author: Andrew Grove

Intel's former chairman and CEO provides his insights on developing a global firm in this business book. We think Grove would choose “management” to describe the talent needed to start and run a business.

That's a skill for CEOs, techies, and data scientists. Grove writes on developing productive teams, motivation, real-life business scenarios, and revolutionizing work.

Five lessons:

Every action is a procedure.

Meetings are a medium of work

Manage short-term goals in accordance with long-term strategies.

Mission-oriented teams accelerate while functional teams increase leverage.

Utilize performance evaluations to enhance output.

So — if the above captures your imagination, it’s well worth getting stuck in.

3. The Hard Thing About Hard Things: Building a Business When There Are No Easy Answers

Author: Ben Horowitz

Few realize how difficult it is to run a business, even though many see it as a tremendous opportunity.

Business schools don't teach managers how to handle the toughest difficulties; they're usually on their own. So Ben Horowitz wrote this book.

It gives tips on creating and maintaining a new firm and analyzes the hurdles CEOs face.

Find suggestions on:

create software

Run a business.

Promote a product

Obtain resources

Smart investment

oversee daily operations

This book will help you cope with tough times.

4. Obviously Awesome: How to Nail Product Positioning

Author: April Dunford

Your job as a data scientist is a product. You should be able to sell what you do to clients. Even if your product is great, you must convince them.

How to? April Dunford's advice: Her book explains how to connect with customers by making your offering seem like a secret sauce.

You'll learn:

Select the ideal market for your products.

Connect an audience to the value of your goods right away.

Take use of three positioning philosophies.

Utilize market trends to aid purchasers

5. The Mom test

Author: Rob Fitzpatrick

The Mom Test improves communication. Client conversations are rarely predictable. The book emphasizes one of the most important communication rules: enquire about specific prior behaviors.

Both ways work. If a client has suggestions or demands, listen carefully and ensure everyone understands. The book is packed with client-speaking tips.

6. Introduction to Machine Learning with Python: A Guide for Data Scientists

Authors: Andreas C. Müller, Sarah Guido

Now, technical documents.

This book is for Python-savvy data scientists who wish to learn machine learning. Authors explain how to use algorithms instead of math theory.

Their technique is ideal for developers who wish to study machine learning basics and use cases. Sci-kit-learn, NumPy, SciPy, pandas, and Jupyter Notebook are covered beyond Python.

If you know machine learning or artificial neural networks, skip this.

7. Python Data Science Handbook: Essential Tools for Working with Data

Author: Jake VanderPlas

Data work isn't easy. Data manipulation, transformation, cleansing, and visualization must be exact.

Python is a popular tool. The Python Data Science Handbook explains everything. The book describes how to utilize Pandas, Numpy, Matplotlib, Scikit-Learn, and Jupyter for beginners.

The only thing missing is a way to apply your learnings.

8. Python for Data Analysis: Data Wrangling with Pandas, NumPy, and IPython

Author: Wes McKinney

The author leads you through manipulating, processing, cleaning, and analyzing Python datasets using NumPy, Pandas, and IPython.

The book's realistic case studies make it a great resource for Python or scientific computing beginners. Once accomplished, you'll uncover online analytics, finance, social science, and economics solutions.

9. Data Science from Scratch

Author: Joel Grus

Here's a title for data scientists with Python, stats, maths, and algebra skills (alongside a grasp of algorithms and machine learning). You'll learn data science's essential libraries, frameworks, modules, and toolkits.

The author works through all the key principles, providing you with the practical abilities to develop simple code. The book is appropriate for intermediate programmers interested in data science and machine learning.

Not that prior knowledge is required. The writing style matches all experience levels, but understanding will help you absorb more.

10. Machine Learning Yearning

Author: Andrew Ng

Andrew Ng is a machine learning expert. Co-founded and teaches at Stanford. This free book shows you how to structure an ML project, including recognizing mistakes and building in complex contexts.

The book delivers knowledge and teaches how to apply it, so you'll know how to:

Determine the optimal course of action for your ML project.

Create software that is more effective than people.

Recognize when to use end-to-end, transfer, and multi-task learning, and how to do so.

Identifying machine learning system flaws

Ng writes easy-to-read books. No rigorous math theory; just a terrific approach to understanding how to make technical machine learning decisions.

11. Deep Learning with PyTorch Step-by-Step

Author: Daniel Voigt Godoy

The last title is also the most recent. The book was revised on 23 January 2022 to discuss Deep Learning and PyTorch, a Python coding tool.

It comprises four parts:

Fundamentals (gradient descent, training linear and logistic regressions in PyTorch)

Machine Learning (deeper models and activation functions, convolutions, transfer learning, initialization schemes)

Sequences (RNN, GRU, LSTM, seq2seq models, attention, self-attention, transformers)

Automatic Language Recognition (tokenization, embeddings, contextual word embeddings, ELMo, BERT, GPT-2)

We admire the book's readability. The author avoids difficult mathematical concepts, making the material feel like a conversation.

Is every data scientist a humanist?

Even as a technological professional, you can't escape human interaction, especially with clients.

We hope these books will help you develop interpersonal skills.

Maria Urkedal York

3 years ago

When at work, don't give up; instead, think like a designer.

How to reframe irritation and go forward

“… before you can figure out where you are going, you need to know where you are, and once you know and accept where you are, you can design your way to where you want to be.” — Bill Burnett and Dave Evans

“You’ve been here before. But there are some new ingredients this time. What can tell yourself that will make you understand that now isn’t just like last year? That there’s something new in this August.”

My coach paused. I sighed, inhaled deeply, and considered her question.

What could I say? I simply needed a plan from her so everything would fall into place and I could be the happy, successful person I want to be.

Time passed. My mind was exhausted from running all morning, all summer, or the last five years, searching for what to do next and how to get there.

Calmer, I remembered that my coach's inquiry had benefited me throughout the summer. The month before our call, I read Designing Your Work Life — How to Thrive and Change and Find Happiness at Work from Standford University’s Bill Burnett and Dave Evans.

A passage in their book felt like a lifeline: “We have something important to say to you: Wherever you are in your work life, whatever job you are doing, it’s good enough. For now. Not forever. For now.”

As I remembered this book on the coaching call, I wondered if I could embrace where I am in August and say my job life is good enough for now. Only temporarily.

I've done that since. I'm getting unstuck.

Here's how you can take the first step in any area where you feel stuck.

How to acquire the perspective of "Good enough for now" for yourself

We’ve all heard the advice to just make the best of a bad situation. That´s not bad advice, but if you only make the best of a bad situation, you are still in a bad situation. It doesn’t get to the root of the problem or offer an opportunity to change the situation. You’re more cheerfully navigating lousiness, which is an improvement, but not much of one and rather hard to sustain over time.” — Bill Burnett and Dave Evans

Reframing Burnett at Evans says good enough for now is the key to being happier at work. Because, as they write, a designer always has options.

Choosing to believe things are good enough for now is liberating. It helps us feel less victimized and less judged. Accepting our situation helps us become unstuck.

Let's break down the process, which designers call constructing your way ahead, into steps you can take today.

Writing helps get started. First, write down your challenge and why it's essential to you. If pen and paper help, try this strategy:

Make the decision to accept the circumstance as it is. Designers always begin by acknowledging the truth of the situation. You now refrain from passing judgment. Instead, you simply describe the situation as accurately as you can. This frees us from negative thought patterns that prevent us from seeing the big picture and instead keep us in a tunnel of negativity.

Look for a reframing right now. Begin with good enough for the moment. Take note of how your body feels as a result. Tell yourself repeatedly that whatever is occurring is sufficient for the time being. Not always, but just now. If you want to, you can even put it in writing and repeatedly breathe it in, almost like a mantra.

You can select a reframe that is more relevant to your situation once you've decided that you're good enough for now and have allowed yourself to believe it. Try to find another perspective that is possible, for instance, if you feel unappreciated at work and your perspective of I need to use and be recognized for all my new skills in my job is making you sad and making you want to resign. For instance, I can learn from others at work and occasionally put my new abilities to use.

After that, leave your mind and act in accordance with your new perspective. Utilize the designer's bias for action to test something out and create a prototype that you can learn from. Your beginning point for creating experiences that will support the new viewpoint derived from the aforementioned point is the new perspective itself. By doing this, you recognize a circumstance at work where you can provide value to yourself or your workplace and then take appropriate action. Send two or three coworkers from whom you wish to learn anything an email, for instance, asking them to get together for coffee or a talk.

Choose tiny, doable actions. You prioritize them at work.

Let's assume you're feeling disconnected at work, so you make a list of folks you may visit each morning or invite to lunch. If you're feeling unmotivated and tired, take a daily walk and treat yourself to a decent coffee.

This may be plenty for now. If you want to take this procedure further, use Burnett and Evans' internet tools and frameworks.

Developing the daily practice of reframing

“We’re not discontented kids in the backseat of the family minivan, but how many of us live our lives, especially our work lives, as if we are?” — Bill Burnett and Dave Evans

I choose the good enough for me perspective every day, often. No quick fix. Am a failing? Maybe a little bit, but I like to think of it more as building muscle.

This way, every time I tell myself it's ok, I hear you. For now, that muscle gets stronger.

Hopefully, reframing will become so natural for us that it will become a habit, and not a technique anymore.

If you feel like you’re stuck in your career or at work, the reframe of Good enough, for now, might be valuable, so just go ahead and try it out right now.

And while you’re playing with this, why not think of other areas of your life too, like your relationships, where you live — even your writing, and see if you can feel a shift?

Hudson Rennie

3 years ago

My Work at a $1.2 Billion Startup That Failed

Sometimes doing everything correctly isn't enough.

In 2020, I could fix my life.

After failing to start a business, I owed $40,000 and had no work.

A $1.2 billion startup on the cusp of going public pulled me up.

Ironically, it was getting ready for an epic fall — with the world watching.

Life sometimes helps. Without a base, even the strongest fall. A corporation that did everything right failed 3 months after going public.

First-row view.

Apple is the creator of Adore.

Out of respect, I've altered the company and employees' names in this account, despite their failure.

Although being a publicly traded company, it may become obvious.

We’ll call it “Adore” — a revolutionary concept in retail shopping.

Two Apple execs established Adore in 2014 with a focus on people-first purchasing.

Jon and Tim:

The concept for the stylish Apple retail locations you see today was developed by retail expert Jon Swanson, who collaborated closely with Steve Jobs.

Tim Cruiter is a graphic designer who produced the recognizable bouncing lamp video that appears at the start of every Pixar film.

The dynamic duo realized their vision.

“What if you could combine the convenience of online shopping with the confidence of the conventional brick-and-mortar store experience.”

Adore's mobile store concept combined traditional retail with online shopping.

Adore brought joy to 70+ cities and 4 countries over 7 years, including the US, Canada, and the UK.

Being employed on the ground floor, with world dominance and IPO on the horizon, was exciting.

I started as an Adore Expert.

I delivered cell phones, helped consumers set them up, and sold add-ons.

As the company grew, I became a Virtual Learning Facilitator and trained new employees across North America using Zoom.

In this capacity, I gained corporate insider knowledge. I worked with the creative team and Jon and Tim.

It's where I saw company foundation fissures. Despite appearances, investors were concerned.

The business strategy was ground-breaking.

Even after seeing my employee stocks fall from a home down payment to $0 (when Adore filed for bankruptcy), it's hard to pinpoint what went wrong.

Solid business model, well-executed.

Jon and Tim's chase for public funding ended in glory.

Here’s the business model in a nutshell:

Buying cell phones is cumbersome. You have two choices:

Online purchase: not knowing what plan you require or how to operate your device.

Enter a store, which can be troublesome and stressful.

Apple, AT&T, and Rogers offered Adore as a free delivery add-on. Customers could:

Have their phone delivered by UPS or Canada Post in 1-2 weeks.

Alternately, arrange for a person to visit them the same day (or sometimes even the same hour) to assist them set up their phone and demonstrate how to use it (transferring contacts, switching the SIM card, etc.).

Each Adore Expert brought a van with extra devices and accessories to customers.

Happy customers.

Here’s how Adore and its partners made money:

Adores partners appreciated sending Experts to consumers' homes since they improved customer satisfaction, average sale, and gadget returns.

**Telecom enterprises have low customer satisfaction. The average NPS is 30/100. Adore's global NPS was 80.

Adore made money by:

a set cost for each delivery

commission on sold warranties and extras

Consumer product applications seemed infinite.

A proprietary scheduling system (“The Adore App”), allowed for same-day, even same-hour deliveries.

It differentiates Adore.

They treated staff generously by:

Options on stock

health advantages

sales enticements

high rates per hour

Four-day workweeks were set by experts.

Being hired early felt like joining Uber, Netflix, or Tesla. We hoped the company's stocks would rise.

Exciting times.

I smiled as I greeted more than 1,000 new staff.

I spent a decade in retail before joining Adore. I needed a change.

After a leap of faith, I needed a lifeline. So, I applied for retail sales jobs in the spring of 2019.

The universe typically offers you what you want after you accept what you need. I needed a job to settle my debt and reach $0 again.

And the universe listened.

After being hired as an Adore Expert, I became a Virtual Learning Facilitator. Enough said.

After weeks of economic damage from the pandemic.

This employment let me work from home during the pandemic. It taught me excellent business skills.

I was active in brainstorming, onboarding new personnel, and expanding communication as we grew.

This job gave me vital skills and a regular paycheck during the pandemic.

It wasn’t until January of 2022 that I left on my own accord to try to work for myself again — this time, it’s going much better.

Adore was perfect. We valued:

Connection

Discovery

Empathy

Everything we did centered on compassion, and we held frequent Justice Calls to discuss diversity and work culture.

The last day of onboarding typically ended in tears as employees felt like they'd found a home, as I had.

Like all nice things, the wonderful vibes ended.

First indication of distress

My first day at the workplace was great.

Fun, intuitive, and they wanted creative individuals, not salesman.

While sales were important, the company's vision was more important.

“To deliver joy through life-changing mobile retail experiences.”

Thorough, forward-thinking training. We had a module on intuition. It gave us role ownership.

We were flown cross-country for training, gave feedback, and felt like we made a difference. Multiple contacts responded immediately and enthusiastically.

The atmosphere was genuine.

Making money was secondary, though. Incredible service was a priority.

Jon and Tim answered new hires' questions during Zoom calls during onboarding. CEOs seldom meet new hires this way, but they seemed to enjoy it.

All appeared well.

But in late 2021, things started changing.

Adore's leadership changed after its IPO. From basic values to sales maximization. We lost communication and were forced to fend for ourselves.

Removed the training wheels.

It got tougher to gain instructions from those above me, and new employees told me their roles weren't as advertised.

External money-focused managers were hired.

Instead of creative types, we hired salespeople.

With a new focus on numbers, Adore's uniqueness began to crumble.

Via Zoom, hundreds of workers were let go.

So.

Early in 2022, mass Zoom firings were trending. A CEO firing 900 workers over Zoom went viral.

Adore was special to me, but it became a headline.

30 June 2022, Vice Motherboard published Watch as Adore's CEO Fires Hundreds.

It described a leaked video of Jon Swanson laying off all staff in Canada and the UK.

They called it a “notice of redundancy”.

The corporation couldn't pay its employees.

I loved Adore's underlying ideals, among other things. We called clients Adorers and sold solutions, not add-ons.

But, like anything, a company is only as strong as its weakest link. And obviously, the people-first focus wasn’t making enough money.

There were signs. The expansion was presumably a race against time and money.

Adore finally declared bankruptcy.

Adore declared bankruptcy 3 months after going public. It happened in waves, like any large-scale fall.

Initial key players to leave were

Then, communication deteriorated.

Lastly, the corporate culture disintegrated.

6 months after leaving Adore, I received a letter in the mail from a Law firm — it was about my stocks.

Adore filed Chapter 11. I had to sue to collect my worthless investments.

I hoped those stocks will be valuable someday. Nope. Nope.

Sad, I sighed.

$1.2 billion firm gone.

I left the workplace 3 months before starting a writing business. Despite being mediocre, I'm doing fine.

I got up as Adore fell.

Finally, can we scale kindness?

I trust my gut. Changes at Adore made me leave before it sank.

Adores' unceremonious slide from a top startup to bankruptcy is astonishing to me.

The company did everything perfectly, in my opinion.

first to market,

provided excellent service

paid their staff handsomely.

was responsible and attentive to criticism

The company wasn't led by an egotistical eccentric. The crew had centuries of cumulative space experience.

I'm optimistic about the future of work culture, but is compassion scalable?

You might also like

Matthew Royse

3 years ago

5 Tips for Concise Writing

Here's how to be clear.

“I have only made this letter longer because I have not had the time to make it shorter.” — French mathematician, physicist, inventor, philosopher, and writer Blaise Pascal

Concise.

People want this. We tend to repeat ourselves and use unnecessary words.

Being vague frustrates readers. It focuses their limited attention span on figuring out what you're saying rather than your message.

Edit carefully.

“Examine every word you put on paper. You’ll find a surprising number that don’t serve any purpose.” — American writer, editor, literary critic, and teacher William Zinsser

How do you write succinctly?

Here are three ways to polish your writing.

1. Delete

Your readers will appreciate it if you delete unnecessary words. If a word or phrase is essential, keep it. Don't force it.

Many readers dislike bloated sentences. Ask yourself if cutting a word or phrase will change the meaning or dilute your message.

For example, you could say, “It’s absolutely essential that I attend this meeting today, so I know the final outcome.” It’s better to say, “It’s critical I attend the meeting today, so I know the results.”

Key takeaway

Delete actually, completely, just, full, kind of, really, and totally. Keep the necessary words, cut the rest.

2. Just Do It

Don't tell readers your plans. Your readers don't need to know your plans. Who are you?

Don't say, "I want to highlight our marketing's problems." Our marketing issues are A, B, and C. This cuts 5–7 words per sentence.

Keep your reader's attention on the essentials, not the fluff. What are you doing? You won't lose readers because you get to the point quickly and don't build up.

Key takeaway

Delete words that don't add to your message. Do something, don't tell readers you will.

3. Cut Overlap

You probably repeat yourself unintentionally. You may add redundant sentences when brainstorming. Read aloud to detect overlap.

Remove repetition from your writing. It's important to edit our writing and thinking to avoid repetition.

Key Takeaway

If you're repeating yourself, combine sentences to avoid overlap.

4. Simplify

Write as you would to family or friends. Communicate clearly. Don't use jargon. These words confuse readers.

Readers want specifics, not jargon. Write simply. Done.

Most adults read at 8th-grade level. Jargon and buzzwords make speech fluffy. This confuses readers who want simple language.

Key takeaway

Ensure all audiences can understand you. USA Today's 5th-grade reading level is intentional. They want everyone to understand.

5. Active voice

Subjects perform actions in active voice. When you write in passive voice, the subject receives the action.

For example, “the board of directors decided to vote on the topic” is an active voice, while “a decision to vote on the topic was made by the board of directors” is a passive voice.

Key takeaway

Active voice clarifies sentences. Active voice is simple and concise.

Bringing It All Together

Five tips help you write clearly. Delete, just do it, cut overlap, use simple language, and write in an active voice.

Clear writing is effective. It's okay to occasionally use unnecessary words or phrases. Realizing it is key. Check your writing.

Adding words costs.

Write more concisely. People will appreciate it and read your future articles, emails, and messages. Spending extra time will increase trust and influence.

“Not that the story need be long, but it will take a long while to make it short.” — Naturalist, essayist, poet, and philosopher Henry David Thoreau

Victoria Kurichenko

3 years ago

My Blog Is in Google's Top 10—Here's How to Compete

"Competition" is beautiful and hateful.

Some people bury their dreams because they are afraid of competition. Others challenge themselves, shaping our world.

Competition is normal.

It spurs innovation and progress.

I wish more people agreed.

As a marketer, content writer, and solopreneur, my readers often ask:

"I want to create a niche website, but I have no ideas. Everything's done"

"Is a website worthwhile?"

I can't count how many times I said, "Yes, it makes sense, and you can succeed in a competitive market."

I encourage and share examples, but it's not enough to overcome competition anxiety.

I launched an SEO writing website for content creators a year ago, knowing it wouldn't beat Ahrefs, Semrush, Backlinko, etc.

Not needed.

Many of my website's pages rank highly on Google.

Everyone can eat the pie.

In a competitive niche, I took a different approach.

Look farther

When chatting with bloggers that want a website, I discovered something fascinating.

They want to launch a website but have no ideas. As a next step, they start listing the interests they believe they should work on, like wellness, lifestyle, investments, etc. I could keep going.

Too many generalists who claim to know everything confuse many.

Generalists aren't trusted.

We want someone to fix our problems immediately.

I don't think broad-spectrum experts are undervalued. People have many demands that go beyond generalists' work. Narrow-niche experts can help.

I've done SEO for three years. I learned from experts and courses. I couldn't find a comprehensive SEO writing resource.

I read tons of articles before realizing that wasn't it. I took courses that covered SEO basics eventually.

I had a demand for learning SEO writing, but there was no solution on the market. My website fills this micro-niche.

Have you ever had trouble online?

Professional courses too general, boring, etc.?

You've bought off-topic books, right?

You're not alone.

Niche ideas!

Big players often disregard new opportunities. Too small. Individual content creators can succeed here.

In a competitive market:

Never choose wide subjects

Think about issues you can relate to and have direct experience with.

Be a consumer to discover both the positive and negative aspects of a good or service.

Merchandise your annoyances.

Consider ways to transform your frustrations into opportunities.

The right niche is half-success. Here is what else I did to hit the Google front page with my website.

An innovative method for choosing subjects

Why publish on social media and websites?

Want likes, shares, followers, or fame?

Some people do it for fun. No judgment.

I bet you want more.

You want to make decent money from blogging.

Writing about random topics, even if they are related to your niche, won’t help you attract an audience from organic search. I'm a marketer and writer.

I worked at companies with dead blogs because they posted for themselves, not readers. They did not follow SEO writing rules; that’s why most of their content flopped.

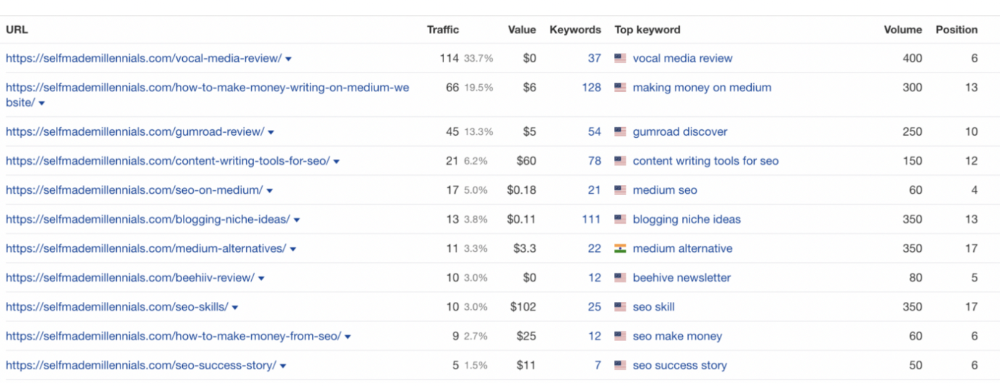

I learned these hard lessons and grew my website from 0 to 3,000+ visitors per month while working on it a few hours a week only. Evidence:

I choose website topics using these criteria:

- Business potential. The information should benefit my audience and generate revenue. There would be no use in having it otherwise.

My topics should help me:

Attract organic search traffic with my "fluff-free" content -> Subscribers > SEO ebook sales.

Simple and effective.

- traffic on search engines. The number of monthly searches reveals how popular my topic is all across the world. If I find that no one is interested in my suggested topic, I don't write a blog article.

- Competition. Every search term is up against rivals. Some are more popular (thus competitive) since more websites target them in organic search. A new website won't score highly for keywords that are too competitive. On the other side, keywords with moderate to light competition can help you rank higher on Google more quickly.

- Search purpose. The "why" underlying users' search requests is revealed. I analyze search intent to understand what users need when they plug various queries in the search bar and what content can perfectly meet their needs.

My specialty website produces money, ranks well, and attracts the target audience because I handpick high-traffic themes.

Following these guidelines, even a new website can stand out.

I wrote a 50-page SEO writing guide where I detailed topic selection and share my front-page Google strategy.

My guide can help you run a successful niche website.

In summary

You're not late to the niche-website party.

The Internet offers many untapped opportunities.

We need new solutions and are willing to listen.

There are unexplored niches in any topic.

Don't fight giants. They have their piece of the pie. They might overlook new opportunities while trying to keep that piece of the pie. You should act now.

Sarah Bird

3 years ago

Memes Help This YouTube Channel Earn Over $12k Per Month

Take a look at a YouTube channel making anything up to over $12k a month from making very simple videos.

And the best part? Its replicable by anyone. Basic videos can be generated for free without design abilities.

Join me as I deconstruct the channel to estimate how much they make, how they do it, and how you can too.

What Do They Do Exactly?

Happy Land posts memes with a simple caption they wrote. So, it's new. The videos are a slideshow of meme photos with stock music.

The site posts 12 times a day.

8-10-minute videos show 10 second images. Thus, each video needs 48-60 memes.

Memes are video titles (e.g. times a boyfriend was hilarious, back to school fails, funny restaurant signs).

Some stats about the channel:

Founded on October 30, 2020

873 videos were added.

81.8k subscribers

67,244,196 views of the video

What Value Are They Adding?

Everyone can find free memes online. This channel collects similar memes into a single video so you don't have to scroll or click for more. It’s right there, you just keep watching and more will come.

By theming it, the audience is prepared for the video's content.

If you want hilarious animal memes or restaurant signs, choose the video and you'll get up to 60 memes without having to look for them. Genius!

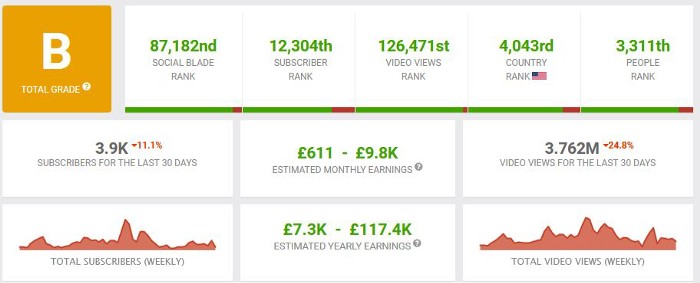

How much money do they make?

According to www.socialblade.com, the channel earns $800-12.8k (image shown in my home currency of GBP).

That's a crazy estimate, but it highlights the unbelievable potential of a channel that presents memes.

This channel thrives on quantity, thus putting out videos is necessary to keep the flow continuing and capture its audience's attention.

How Are the Videos Made?

Straightforward. Memes are added to a presentation without editing (so you could make this in PowerPoint or Keynote).

Each slide should include a unique image and caption. Set 10 seconds per slide.

Add music and post the video.

Finding enough memes for the material and theming is difficult, but if you enjoy memes, this is a fun job.

This case study should have shown you that you don't need expensive software or design expertise to make entertaining videos. Why not try fresh, easy-to-do ideas and see where they lead?